5,49 €

Mehr erfahren.

- Herausgeber: After Midnight Publishing

- Kategorie: Fachliteratur

- Sprache: Englisch

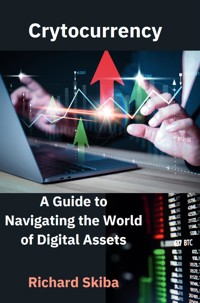

Explore the dynamic world of cryptocurrency with this comprehensive guide, which begins with fundamental concepts and advances to complex topics. The book introduces cryptocurrency, covering its definition, historical development, and core principles like decentralization, blockchain technology, and cryptography. It then delves into Bitcoin’s origins, including the enigmatic Satoshi Nakamoto, the mechanics behind Bitcoin, and the intricacies of Bitcoin mining.

The guide continues with a detailed examination of blockchain technology, including its structure, transaction processes, and consensus mechanisms such as Proof of Work and Proof of Stake, along with an analysis of security and anonymity. It explores major cryptocurrencies beyond Bitcoin, like Ethereum, Ripple, and Litecoin, and examines emerging altcoins.

Readers will learn about cryptocurrency wallets and exchanges, the differences between hot and cold wallets, asset security, and exchange selection. Investment strategies are discussed, comparing technical and fundamental analysis, and addressing portfolio diversification, risks, and rewards.

The book also covers legal and regulatory issues, real-world applications like DeFi and NFTs, and provides insights on security and fraud prevention. It concludes with a look at cryptocurrency mining, smart contracts, societal impacts, and practical advice on creating new cryptocurrencies and ETFs.

This guide is ideal for beginners, investors, tech enthusiasts, regulators, and developers, offering valuable insights tailored to each audience.

Das E-Book können Sie in Legimi-Apps oder einer beliebigen App lesen, die das folgende Format unterstützen:

Veröffentlichungsjahr: 2024

Ähnliche

Cryptocurrency

A Guide to Navigating the World of Digital Assets

Richard Skiba

Copyright © 2024 by Richard Skiba

All rights reserved.

No portion of this book may be reproduced in any form without written permission from the publisher or author, except as permitted by copyright law.

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional when appropriate. Neither the publisher nor the author shall be liable for any loss of profit or any other commercial damages, including but not limited to special, incidental, consequential, personal, or other damages.

Skiba, Richard (author)

Cryptocurrency: A Guide to Navigating the World of Digital Assets

ISBN 978-1-7636112-8-3 (paperback) 978-1-7636112-9-0 (eBook)

Non-fiction

Contents

Introduction to Cryptocurrency

What is Cryptocurrency?

Cryptocurrencies are digital or virtual forms of currency secured by cryptography, operating independently of central authorities and utilizing decentralized technologies like blockchain [1]. This decentralization eliminates the need for intermediaries like banks, enabling global accessibility and transactions without geographical boundaries [2]. The security of cryptocurrencies is ensured through cryptographic techniques that safeguard transactions and control the creation of new units, making them resistant to fraud and counterfeiting [3]. While transactions are recorded on a public ledger, the identities of parties involved are often pseudonymous, offering a degree of anonymity [4].

Cryptocurrency, often referred to as crypto, is a digital or virtual form of currency that relies on cryptography for security. Unlike traditional currencies issued and regulated by governments, cryptocurrencies operate on decentralized networks, typically based on blockchain technology. Cryptocurrencies function by [5]:

Digital and Decentralized Nature: Cryptocurrencies exist purely in digital form and do not have a physical counterpart like coins or banknotes. They operate on decentralized networks, which means there is no central authority or institution controlling them. Instead, transactions and the issuance of new units are managed collectively by the network of users.

Peer-to-Peer Transactions: Cryptocurrencies enable direct peer-to-peer transactions without the need for intermediaries like banks. Transactions are verified and recorded in a public ledger called the blockchain, which is maintained by participants in the network.

Security through Cryptography: Cryptography plays a crucial role in ensuring the security of cryptocurrency transactions. It involves advanced mathematical techniques for encrypting data, which secures the transfer of funds and the integrity of the transaction records.

Public Ledger (Blockchain): The blockchain is a decentralized and distributed ledger that records all transactions across the network. Each transaction is verified by network nodes through cryptographic algorithms and added to the blockchain in a chronological order. This transparency and immutability make blockchain a trusted system for recording transactions.

Mining and Creation of Cryptocurrency: New units of cryptocurrencies are typically created through a process called mining. Mining involves solving complex mathematical puzzles using computational power. Miners compete to validate transactions and are rewarded with newly minted coins. This process also helps to secure the network and verify transactions.

Cryptocurrency Wallets: Cryptocurrencies are stored in digital wallets, which can be software applications, hardware devices, or even paper copies that store public and private keys. These keys are essential for accessing and managing cryptocurrency holdings securely.

Speculation and Investment: Cryptocurrencies have gained popularity not only for their potential as a medium of exchange but also as speculative assets. Price volatility and speculative trading have contributed to their appeal as investment vehicles.

Future Applications: Beyond financial transactions, blockchain technology, which underpins cryptocurrencies, has the potential to revolutionize various industries. It could be used for trading financial assets like bonds and stocks, supply chain management, voting systems, and more, leveraging its transparency, security, and efficiency.

Cryptocurrencies have diversified significantly since the introduction of Bitcoin in 2009 [5]. Here's a detailed exploration of some prominent examples [5]:

Bitcoin:

Introduction: Bitcoin, launched in 2009 by an anonymous entity known as Satoshi Nakamoto, marked the beginning of cryptocurrencies. It operates on a decentralized peer-to-peer network, using blockchain technology to secure transactions.

Key Features: Bitcoin is known for its limited supply (capped at 21 million coins), its role as a store of value, and its widespread acceptance as a digital currency. It remains the most widely recognized and traded cryptocurrency globally.

Ethereum:

Introduction: Created in 2015 by Vitalik Buterin, Ethereum is not just a cryptocurrency but a decentralized platform that enables developers to build and deploy smart contracts and decentralized applications (DApps).

Key Features: Ethereum's cryptocurrency is called Ether (ETH). It differs from Bitcoin in that it facilitates more complex transactions beyond simple peer-to-peer payments. Ethereum's blockchain supports programmable contracts and has become a foundation for various blockchain-based innovations.

Litecoin:

Introduction: Introduced in 2011 by Charlie Lee, Litecoin is often referred to as the "silver to Bitcoin's gold." It was designed to provide faster transaction confirmation times and a different hashing algorithm (Scrypt) compared to Bitcoin's SHA-256.

Key Features: Litecoin aims to be a more efficient cryptocurrency for smaller transactions and day-to-day use. It shares many technological similarities with Bitcoin but has implemented certain improvements to enhance usability and transaction speed.

Ripple (XRP):

Introduction: Ripple was launched in 2012 by Ripple Labs Inc. as both a payment protocol and a digital currency (XRP). Unlike Bitcoin and Ethereum, Ripple focuses on facilitating fast and low-cost cross-border payments and settlements.

Key Features: Ripple's consensus ledger, known as the XRP Ledger, does not require mining like Bitcoin and uses a consensus protocol to validate transactions. It has gained attention for its partnerships with financial institutions and its potential to disrupt traditional banking systems.

Altcoins:

Definition: Altcoins refer to all cryptocurrencies other than Bitcoin. They encompass a vast array of digital currencies, each with its own unique features and purposes.

Diversity: Altcoins include thousands of cryptocurrencies, each designed with specific goals in mind, such as enhancing privacy (e.g., Monero), facilitating smart contracts (e.g., Cardano), or serving niche communities.

General Characteristics:

Decentralization: Most cryptocurrencies operate on decentralized networks, reducing reliance on central authorities.

Cryptographic Security: All cryptocurrencies use cryptography to secure transactions and control the creation of new units.

Global Accessibility: Cryptocurrencies enable global transactions without the need for intermediaries, offering financial inclusion to unbanked populations.

Cryptocurrency's utility as a medium of exchange has evolved since Bitcoin's inception, though its widespread adoption for everyday transactions remains a work in progress. Here's a detailed exploration of what you can currently buy with cryptocurrency and how its use has expanded [5]:

Technology and E-commerce Sites:

Newegg.com, AT&T, Microsoft: These tech giants accept cryptocurrency payments on their websites, allowing customers to purchase a variety of tech products and services using Bitcoin and sometimes other cryptocurrencies.

Overstock, Shopify, Rakuten, Home Depot: Overstock was one of the pioneers in accepting Bitcoin for online purchases. Shopify and Rakuten have also integrated cryptocurrency payments, while Home Depot has explored similar avenues, broadening the scope of goods available for purchase with crypto.

Luxury Goods:

Bitdials: This online luxury retailer specializes in high-end watches like Rolex and Patek Philippe, offering them in exchange for Bitcoin. Luxury goods are increasingly becoming accessible to crypto holders looking to diversify their portfolios or make extravagant purchases.

Cars:

Car Dealers: From mainstream automotive brands to high-end luxury dealerships, some car dealerships have embraced cryptocurrency as a payment option. This includes both new and used cars, reflecting a growing trend in the automotive sector towards digital payments.

Insurance:

AXA: In April 2021, Swiss insurer AXA announced its acceptance of Bitcoin for insurance premium payments across various insurance lines, except for life insurance due to regulatory constraints. This move underscores cryptocurrency's potential utility in sectors traditionally reliant on fiat currencies.

Premier Shield Insurance: This US-based insurer allows policyholders to pay for home and auto insurance using Bitcoin, providing flexibility and convenience for crypto holders seeking insurance coverage.

Cryptocurrency Debit Cards:

BitPay: For consumers looking to spend cryptocurrency at retailers that do not directly accept digital currencies, cryptocurrency debit cards like BitPay offer a solution. These cards convert cryptocurrency holdings into fiat currency at the point of sale, enabling seamless transactions at millions of merchants worldwide.

While the adoption of cryptocurrency for everyday purchases has seen significant strides, challenges remain, including price volatility, regulatory uncertainties, and integration complexities for merchants. Despite these hurdles, the expanding list of industries and companies accepting cryptocurrency illustrates its growing acceptance and integration into global commerce. As technology advances and consumer demand evolves, the future of cryptocurrency as a viable alternative to traditional payment methods continues to unfold.

A Bitcoin ATM or bitcoin teller machine (BTM) currently found in Ave. BU-5, Santa Juanita, Bayamón, Puerto Rico 00960, inside Puma Gas Station. PuertoCrypto, CC0, via Wikimedia Commons.

Buying cryptocurrency involves several steps to ensure safety and efficiency. Here’s a detailed explanation of how to buy cryptocurrency [5]:

Step 1: Choosing a Platform

The first step is selecting a platform where you can buy and trade cryptocurrencies. You typically have two main options:

Traditional Brokers: These online brokers offer a range of financial assets, including cryptocurrencies, alongside stocks, bonds, and ETFs. They often have lower trading costs but may provide fewer crypto-specific features.

Cryptocurrency Exchanges: These platforms specialize in buying, selling, and trading cryptocurrencies. They offer a wide variety of digital assets, wallet storage solutions, interest-bearing accounts, and more. However, they may charge higher fees compared to traditional brokers.

When choosing a platform, consider the following factors [5]:

Cryptocurrency Selection: Check which cryptocurrencies are available for trading.

Fees: Compare trading fees, deposit and withdrawal fees, and any other charges associated with the platform.

Security: Look for platforms with robust security measures, such as two-factor authentication (2FA) and cold storage options for funds.

Payment Methods: Evaluate accepted payment methods, such as debit/credit cards, ACH transfers, and wire transfers.

User Interface: Assess the platform’s usability, including its web and mobile interfaces.

Regulatory Compliance: Ensure the platform operates within regulatory frameworks to protect your investments.

Step 2: Funding Your Account

Once you’ve chosen a platform, the next step is to fund your account to start trading cryptocurrencies. Methods for funding your account typically include:

Debit/Credit Cards: Many exchanges allow you to purchase cryptocurrencies directly using fiat currencies (e.g., USD, EUR, GBP) via debit or credit cards. Note that some credit card companies may restrict cryptocurrency transactions due to their volatility.

ACH Transfers: Some platforms support ACH transfers for depositing funds from your bank account.

Wire Transfers: Direct wire transfers are another common method for funding accounts, especially for larger amounts.

Each funding method may have different processing times and associated fees, so it’s essential to review these details carefully before proceeding.

Step 3: Placing an Order

Once your account is funded, you can place an order to buy cryptocurrency:

Order Placement: Navigate to the trading section of your chosen platform (web or mobile), select the cryptocurrency you wish to purchase, and specify the amount.

Order Types: Choose from different order types such as market orders (executed immediately at the current market price) or limit orders (executed only when the price reaches a specified level).

Confirmation: Review your order details, including fees and total cost, before confirming the purchase.

Alternative Investment Vehicles

Beyond direct purchases on exchanges, there are alternative ways to invest in cryptocurrencies:

Payment Services: Platforms like PayPal, Cash App, and Venmo allow users to buy, sell, or hold cryptocurrencies within their apps.

Bitcoin Trusts and ETFs: These investment vehicles enable indirect exposure to cryptocurrencies through traditional brokerage accounts, offering shares tied to the value of Bitcoin or other digital assets.

Blockchain Stocks or ETFs: Invest indirectly in cryptocurrencies by purchasing stocks or ETFs of companies involved in blockchain technology development or cryptocurrency transactions.

Choosing the best investment approach depends on your financial goals, risk tolerance, and preferred method of investment. Whether you opt for direct crypto exchanges or indirect investments through traditional financial products, understanding the risks and benefits is crucial for making informed decisions in the evolving cryptocurrency market.

Storing cryptocurrency securely is crucial to protect your digital assets from hacks and theft. Here’s a detailed explanation of how to store cryptocurrency [5]:

Cryptocurrency wallets are digital tools that store your private keys, which are essential for accessing and managing your cryptocurrencies. Private keys are unique cryptographic keys that allow you to authorize transactions on the blockchain network associated with each cryptocurrency.

Types of Cryptocurrency Wallets

Hot Wallets:

Definition: Hot wallets are software-based wallets that store your private keys online, typically provided by cryptocurrency exchanges or accessed through online platforms.

Accessibility: Convenient for frequent trading and transactions due to immediate access via the internet.

Security: Vulnerable to hacking and cyberattacks since they are connected to the internet.

Examples: Wallets provided by exchanges like Coinbase, Binance, or software wallets such as Electrum or MyEtherWallet.

Cold Wallets (Hardware Wallets):

Definition: Cold wallets are physical devices designed to store private keys offline, providing a higher level of security.

Security: Offers protection against online threats such as hacking because private keys are stored offline.

Usage: Ideal for long-term storage of significant amounts of cryptocurrency that you don’t plan to trade frequently.

Examples: Ledger Nano S, Ledger Nano X, Trezor Model T.

Steps to Store Cryptocurrency Safely

Choose a Wallet Provider:

Research and select a reputable wallet provider that offers the type of storage (hot or cold) that suits your needs.

Consider factors such as security features, user interface, supported cryptocurrencies, and customer support.

Set Up Your Wallet:

Follow the provider’s instructions to create and set up your wallet account.

Generate and securely store your recovery seed phrase. This phrase is crucial for recovering access to your wallet if you forget your password or lose access.

Transfer Your Cryptocurrency:

If your cryptocurrency is currently stored on an exchange or another wallet, initiate a transfer to your newly set up wallet.

Ensure you enter the correct wallet address and verify the transaction details before confirming.

Security Best Practices:

Enable Two-Factor Authentication (2FA): Add an extra layer of security to your wallet account by enabling 2FA wherever possible.

Keep Software Updated: Regularly update your wallet software to protect against vulnerabilities and security threats.

Use Strong Passwords: Create strong, unique passwords for your wallet accounts and avoid using easily guessable information.

Regular Backups:

Backup your wallet regularly, especially if it’s a software wallet. Store backups securely in multiple locations (e.g., encrypted USB drives, offline storage) to prevent data loss.

Monitor Your Accounts:

Regularly monitor your wallet accounts and transactions for any unauthorized activity.

Stay informed about security best practices and updates from your wallet provider.

Cryptocurrency fraud and scams have unfortunately become prevalent as the popularity of digital currencies has risen. Here’s a detailed explanation of the types of cryptocurrency fraud and scams, as well as safety measures and tips for investing safely [5]:

Types of Cryptocurrency Scams

Fake Websites:

Description: Fraudulent websites mimic legitimate cryptocurrency exchanges or investment platforms. They use fake testimonials and promises of guaranteed high returns to lure unsuspecting investors.

Risk: Investors who deposit funds into these fake platforms often lose their money entirely, as the scammers disappear once they’ve collected enough funds.

Virtual Ponzi Schemes:

Description: Similar to traditional Ponzi schemes, cryptocurrency Ponzi schemes promise high returns to investors. New investor funds are used to pay returns to earlier investors, creating a cycle of apparent profitability until the scheme collapses.

Example: BitClub Network, which defrauded investors of over $700 million before its operators were apprehended in 2019.

Celebrity Endorsements and Rumours:

Description: Scammers impersonate celebrities or influential figures online, claiming endorsement of a particular cryptocurrency. They create false hype to inflate the price, allowing them to sell off their holdings at a profit before the scheme is exposed.

Risk: Investors who buy into these rumours often suffer losses when the price crashes after the scam is revealed.

Romance Scams:

Description: Scammers build relationships with victims on dating apps or social media platforms, then persuade them to invest in cryptocurrencies. The victims transfer funds to the scammer’s account, believing they are investing, but end up losing their money.

Statistics: The FBI received over 1,800 reports of crypto-focused romance scams in the first seven months of 2021, resulting in $133 million in losses.

Fake Exchanges and Traders:

Description: Fraudsters set up fake cryptocurrency exchanges or pose as legitimate traders offering unrealistic returns on investments.

Risk: Investors who deposit funds or trade with these fraudulent entities risk losing their investments entirely, as these operations are designed solely to defraud.

Cryptocurrency Hacking:

Description: Hackers target cryptocurrency exchanges and wallets to steal digital assets. They exploit vulnerabilities in security systems or use phishing attacks to gain access to private keys.

Examples: Notable hacks include Coincheck losing $534 million and BitGrail losing $195 million in 2018.

Safety Measures and Tips for Investing in Cryptocurrency

Choose Reputable Exchanges:

Research and select well-established cryptocurrency exchanges with strong security measures and a good reputation. Read reviews and consider recommendations from experienced investors.

Use Secure Wallets:

Preferably use hardware wallets (cold wallets) to store large amounts of cryptocurrency securely offline. Alternatively, use reputable software wallets (hot wallets) with strong security features.

Educate Yourself:

Understand the basics of blockchain technology, how cryptocurrencies work, and the risks involved in investing.

Stay informed about common scams and fraud tactics to recognize warning signs.

Diversify Your Investments:

Spread your investments across different cryptocurrencies to mitigate risk. Avoid putting all your funds into one asset, such as Bitcoin, despite its popularity.

Prepare for Volatility:

Cryptocurrency prices can be highly volatile, leading to substantial gains or losses. Only invest funds that you can afford to lose without affecting your financial stability.

Be Cautious of Unrealistic Promises:

Avoid investments promising guaranteed high returns or endorsed by celebrities without thorough verification.

Verify information independently and avoid succumbing to FOMO (Fear of Missing Out) induced by social media hype.

Security Practices:

Enable two-factor authentication (2FA) on all accounts associated with cryptocurrency transactions.

Use strong, unique passwords and keep them secure. Regularly update software and firmware on wallets and devices.

One of the key features of cryptocurrencies is their limited supply, with many having a capped maximum number of coins or tokens that can ever be created, enforced through embedded protocols in the cryptocurrency's code [6]. Beyond simple transactions, cryptocurrencies serve various purposes such as facilitating smart contracts, decentralized applications (DApps), and tokenization of assets [7]. Bitcoin, introduced in 2009 as the first decentralized cryptocurrency by an anonymous entity known as Satoshi Nakamoto, remains the most well-known in the market [8]. Since then, thousands of other cryptocurrencies, often referred to as altcoins, have been created, each with unique features and applications [9].

The integration of cryptocurrencies, particularly Bitcoin, into retirement savings plans has gained significant attention, highlighting the growing acceptance and adoption of digital assets in traditional financial systems [10]. Cryptocurrencies operate on decentralized networks, typically utilizing blockchain technology to ensure transparency, security, and immutability of transactions [11]. The emergence of cryptocurrencies has challenged conventional banking systems and monetary policies, offering advantages to overcome limitations in traditional financial systems [12]. Despite the advantages, debates exist around the security of cryptocurrencies due to the lack of authoritative control, raising concerns about their safety and reliability [13].

The high volatility and inherent risk associated with cryptocurrency investments have prompted studies to analyse the determinants of value perception and factors influencing individuals' intentions regarding cryptocurrency adoption and investment decisions [14]. Cryptocurrencies have been identified as a new form of digital asset that functions through blockchain technology, aiming to serve as an instrument of exchange [15]. The global nature of cryptocurrencies allows for potentially more secure and lower-cost transfers accessible to individuals in remote regions through smartphones [16]. Blockchain technology, fundamental to the popularity of cryptocurrencies, has also been recognized for its potential in enhancing supply chain performance and logistics management [17].

Research has shown that cryptocurrencies like Bitcoin have impacted the current financial legal landscape, emphasizing the increasing importance of regulating these digital assets [18]. The rise of cryptocurrency adoption in various regions, including Pakistan, has been facilitated by the establishment of crypto exchanges, educational initiatives, and supporting infrastructure [19]. The impact of monetary systems on income inequality and wealth distribution has been explored, suggesting that utilizing cryptocurrency systems could promote economic equality by providing equal access to finance and investment opportunities [20]. Additionally, studies have quantified the sustainability of Bitcoin and blockchain technologies, highlighting the need to assess the environmental impact and long-term viability of these digital assets [21].

Cryptocurrencies represent a transformative force in the global financial landscape, offering decentralized, secure, and efficient means of transactions and asset management. The adoption and acceptance of cryptocurrencies continue to grow, challenging traditional financial systems and prompting regulatory considerations to ensure their sustainable integration into the economy. As the market evolves and technologies advance, further research and analysis will be crucial in understanding the implications, risks, and opportunities presented by cryptocurrencies in the modern financial ecosystem.

Cryptocurrency's classification as 'money' is a topic of debate, often assessed against the key characteristics that define traditional forms of money [22]:

Widely Accepted Means of Payment: Money is typically recognized and accepted universally within a nation's economy for transactions. While cryptocurrencies can be used for buying and selling goods and services, their acceptance remains limited compared to national currencies. Surveys indicate that only a small percentage of cryptocurrency holders regularly use them for daily transactions, indicating a lack of widespread acceptance.

Store of Value: Money should retain its purchasing power over time, allowing it to serve as a reliable store of value. Cryptocurrencies, however, are known for their price volatility. Significant fluctuations in value can occur rapidly, making it challenging for cryptocurrencies to maintain stable purchasing power. This volatility undermines their effectiveness as a store of value compared to more stable forms of money.

Unit of Account: Money serves as a standard measure for pricing goods and services within an economy. In many countries, prices are quoted and transactions conducted in the national currency (e.g., Australian dollars). While some businesses accept cryptocurrencies as payment, they are not commonly used as a unit of account. This means cryptocurrencies are not widely adopted for everyday price comparisons or financial reporting.

Given these criteria, cryptocurrencies currently do not fully meet the standards typically associated with traditional money. They can function as a means of payment in certain contexts but lack broad acceptance, price stability, and widespread use as a unit of account [22].

It's worth noting that central banks are exploring the concept of digital currencies issued by themselves, often referred to as central bank digital currencies (CBDCs). Unlike cryptocurrencies, CBDCs would be issued and regulated by a central authority, potentially offering characteristics more aligned with traditional money, such as stability and official recognition within the financial system. Therefore, while cryptocurrencies have characteristics of money to some extent, they do not meet all the criteria required for broader recognition as a mainstream form of money [22].

A Central Bank Digital Currency (CBDC) represents a digital form of sovereign currency issued and regulated by a country's central bank. Unlike cryptocurrencies, which are decentralized and operate independently of any central authority, CBDCs are backed by the full faith and credit of the issuing government. They are designed to function similarly to physical cash but in a digital form, providing a secure and regulated means of conducting transactions within an economy [22].

One of the fundamental aspects distinguishing CBDCs from cryptocurrencies is their legal tender status. As an official form of currency, CBDCs would be universally accepted as a means of payment, just like physical cash or electronic bank deposits. This acceptance ensures that CBDCs can be used for various transactions, from everyday purchases to large-scale financial settlements, across the entire economy [22].

Another critical difference lies in the stability and reliability of CBDCs as a store of value. Unlike many cryptocurrencies, which are notorious for their price volatility driven by market speculation and demand, CBDCs would be designed to maintain stable purchasing power. This stability is crucial for fostering confidence among users and businesses, supporting financial planning, and facilitating economic transactions without the risk of significant value fluctuations [22].

Furthermore, CBDCs would serve as a standard unit of account within their respective economies. For example, a CBDC issued by the Reserve Bank would be denominated in Australian dollars, allowing it to serve as a consistent measure for pricing goods and services. This characteristic enhances the efficiency of economic transactions, simplifies accounting and financial reporting, and promotes price transparency across sectors [22].

Cryptocurrency Transactions

Cryptocurrency transactions operate through electronic messages within a decentralized network, employing blockchain technology for confirmation and security. The process begins when Alice initiates a transaction by sending a message containing the recipient's electronic address (public key), the amount of cryptocurrency to be transferred, and a timestamp indicating the transaction's initiation [22].

Once initiated, Alice's transaction is broadcasted across all nodes participating in the cryptocurrency network. Each node maintains a complete ledger of all transactions ever conducted, known as the blockchain. Transactions, including Alice's, enter a transaction pool (mempool), awaiting validation and inclusion in a new block [22].

Miners, specialized participants with powerful computers, compete to solve a complex cryptographic puzzle based on pending transactions. The first miner to solve the puzzle creates a new block, incorporating Alice's transaction along with others from the mempool.

Upon solving the puzzle, the miner broadcasts the newly created block to the network. Other nodes verify the block's validity, ensuring all transactions within it are legitimate and that the cryptographic proof of work provided by the miner is accurate. Consensus among nodes is crucial, achieved through mechanisms like Proof of Work (PoW), confirming the block's authenticity [22].

Once validated and accepted by the network, the new block is appended to the end of the blockchain. This blockchain serves as a decentralized and immutable ledger, sequentially recording all transactions conducted within the cryptocurrency network. Alice's transaction is now confirmed and permanently added to the blockchain record.

Confirmation of a transaction like Alice's occurs relatively quickly upon inclusion in a block. However, for enhanced security and irreversibility, it is common practice in blockchain networks, such as Bitcoin, to wait for multiple subsequent blocks to be added on top of the block containing Alice's transaction. This process, often requiring six additional blocks, ensures that the transaction is deeply buried within the blockchain, making it computationally impractical and highly secure to reverse. Thus, ensuring finality and trust in cryptocurrency transactions [22].

History of Digital Currency

The history of digital currency traces back several decades, characterized by transformative technological advancements and paradigm shifts in finance. Here’s a detailed chronological overview of its key milestones.

In the 1980s and early 1990s, a significant period in the development of digital cash systems and cryptographic protocols occurred before the widespread use of the Internet. David , an American cryptographer, made notable contributions during this era by introducing innovative concepts related to anonymous digital cash and cryptographic protocols [23]. 's work was foundational in establishing secure digital transactions, envisioning a future where financial privacy and security could be greatly enhanced through digital means. Companies like DigiCash and CyberCash emerged as pioneers in electronic money during the 1990s, with DigiCash, founded by , creating eCash, one of the earliest forms of digital currency backed by real-world currencies [23].

Chaum's extensive work on unconditionally anonymous protocols aimed to create the digital equivalent of cash, ensuring anonymity and security in transactions [23]. His vision of security without identification in transaction systems provided a practical solution to privacy concerns, aiming to render concepts like "Big Brother" obsolete [24]. The development of digital cash schemes involved cryptographic protocols for withdrawal, transfer, deposit, and division, meeting the security and anonymity needs of all participants [25]. These schemes were designed to prevent undetected reuse or forgery, offering assurance of authenticity for customers and banks [25].

The concept of digital cash and cryptographic protocols is closely linked to the idea of usage-based pricing and digital transactions, as explored by Mackie-Mason and Varian [26]. The emergence of digital cash systems necessitated innovative cryptographic tools and methodologies [27]. Their research focused on methodologies for off-line digital cash using general cryptographic tools, underscoring the importance of robust cryptographic foundations in ensuring the security and integrity of digital transactions [27].

Moreover, witness hiding proofs and applications, such as those discussed by Chen [28], significantly enhanced the security of electronic cash systems. Witness hiding proofs were crucial for applications like electronic cash and digital signatures, ensuring the confidentiality and integrity of transactions [28]. The integration of digital cash into multiparty protocols, enabled by verifiable signature sharing as discussed Franklin & Reiter [29], facilitated secure distributed auctions and cash escrow services, further enhancing the utility and security of digital cash systems.

In the field of cryptography, the RSA algorithm, utilized in applied cryptography protocols [30], played a vital role in securing digital transactions. Robust cryptographic algorithms like RSA were essential for safeguarding the confidentiality and integrity of digital cash systems [30]. Additionally, the development of privacy-protecting off-line electronic cash systems challenged the notion that such systems must be based on blind signature issuing protocols, as highlighted by Brands [31]. This research debunked the popular belief, emphasizing the importance of diverse cryptographic approaches in ensuring the privacy and security of electronic cash systems [31].

Overall, the Pre-Internet Era of the 1980s and early 1990s witnessed a transformative period in the development of digital cash systems and cryptographic protocols. Visionaries like David Chaum and pioneering companies such as DigiCash laid the groundwork for secure and anonymous digital transactions, shaping the future of financial privacy and security in the digital age.

The 1990s and early 2000s saw the emergence of pioneering digital currency initiatives like DigiCash and CyberCash, which faced challenges leading to their closure. These early ventures highlighted the significant hurdles in integrating digital currencies into traditional financial systems and gaining widespread consumer acceptance. Regulatory uncertainties, technological constraints, and market reception were significant obstacles during this period [32].

The concept of digital money predates Bitcoin, with its origins dating back to the 1980s and 1990s, exemplified by projects such as David Chaum's DigiCash and Wei Dai's b-money [32]. These early experiments laid the foundation for the development of digital currencies and emphasized the complexities involved in establishing these innovative forms of financial transactions within existing frameworks.

As digital currencies evolved, research explored their features, functions, and potential impacts on the financial landscape. Studies have compared digital currencies with traditional fiat currencies, highlighting the advantages and disadvantages inherent in these new forms of monetary exchange [33]. Understanding these differences is crucial for policymakers, financial institutions, and consumers navigating the changing landscape of digital finance.

The development of digital currencies has not been without challenges. Issues such as data security and vulnerabilities to cyber-attacks have been scrutinized, underscoring the importance of protecting digital assets in an increasingly interconnected financial ecosystem [34]. Addressing these security concerns is essential for building trust and confidence in digital currency systems.

Furthermore, the rise of digital currencies has sparked discussions on their implications for economic sanctions and regulatory frameworks. The decentralized nature of cryptocurrencies has raised concerns about potential risks of sanction evasion, leading to diverse regulatory approaches globally [35]. Balancing innovation with regulatory oversight is a critical consideration in the ongoing evolution of digital currencies.

At the core of discussions on digital currencies is the role of central banks and their potential issuance of digital currencies. The introduction of central bank digital currencies (CBDCs) has initiated debates on their impact on existing cryptocurrencies and the broader financial landscape [36]. Understanding the dynamics between CBDCs and private digital currencies is crucial for anticipating potential shifts in the monetary system.

The adoption of digital currencies has been studied in various regions, providing insights into the different drivers, challenges, and success stories across different contexts. Research has examined digital currency adoption in Africa, offering unique perspectives on the global landscape of digital finance [37]. These analyses offer valuable insights into the diverse paths of digital currency integration worldwide.

Moreover, the intersection of digital currencies with financial inclusion has been a key focus of research. Scholars have explored how central bank digital currencies could enhance financial access for underserved populations [36]. By investigating the connection between digital currencies and financial inclusion, researchers aim to identify ways to leverage these technologies to bridge economic disparities.

In the context of the evolving monetary system, the emergence of digital currencies has prompted reflections on their impact on traditional banking sectors. Studies have analysed how digital currencies influence banking operations in Europe, highlighting the transformative potential of these technologies [38]. Understanding the implications of digital currencies on banking institutions is crucial for navigating the changing financial landscape.

As digital currencies gain momentum, discussions on their legal governance and regulatory frameworks have become increasingly relevant. Scholars have stressed the importance of establishing clear legal frameworks for digital currencies to mitigate risks such as money laundering and data breaches [39]. Developing robust regulatory mechanisms is essential for creating a secure and stable environment for digital financial transactions.

The period from the 1990s to the early 2000s witnessed the early stages of digital currency development, characterized by innovation and challenges. The experiences of pioneering ventures like DigiCash and CyberCash laid the groundwork for subsequent advancements in digital finance. As researchers delve into the intricacies of digital currencies, addressing issues related to regulation, security, and adoption will be crucial in shaping the future trajectory of financial systems.

The emergence of Bitcoin in 2008 marked a significant milestone in the realm of digital currencies and blockchain technology. Satoshi Nakamoto introduced Bitcoin through a whitepaper that outlined a decentralized digital currency system [40]. This system leveraged blockchain technology to enable peer-to-peer transactions without the need for intermediaries like banks [41]. The release of this whitepaper was a pivotal moment, setting the stage for the first Bitcoin transaction in January 2009, which initiated the Bitcoin blockchain and the issuance of bitcoins as its native cryptocurrency [42].

Nakamoto's whitepaper described Bitcoin as a peer-to-peer cash system where a network of nodes verified transactions to prevent double-spending, laying the foundation for the decentralized and trustless nature of Bitcoin transactions [41]. This innovative concept of a decentralized, distributed, and cryptographically secured ledger formed the basis of Bitcoin and subsequent blockchain-based systems [40]. The whitepaper introduced a protocol with robust cryptographic security, emphasizing the birth of Bitcoin as a groundbreaking digital currency [40].

The impact of Nakamoto's whitepaper extended beyond the creation of Bitcoin, influencing the broader adoption of blockchain technology in various sectors. The whitepaper not only introduced Bitcoin but also catalysed the development of blockchain technology, which has since found applications in fields like agriculture, finance, and supply chain management [43]. The success of Bitcoin as the first application of blockchain technology sparked debates in banking and finance sectors, with some considering it a potential successor to traditional fiat currency systems [44].

The whitepaper's release in 2008 paved the way for the development of blockchain technology, which has evolved into a widely adopted innovation in modern society [45]. Blockchain's architectural design, characterized by distributed and encrypted data storage, has enabled secure and transparent transactions across various industries [42]. The decentralized nature of blockchain technology has led to the creation of diverse applications beyond cryptocurrencies, including smart contracts, decentralized finance, and supply chain management systems [46].

Furthermore, the whitepaper's emphasis on decentralization, trustlessness, and cryptographic security laid the groundwork for the emergence of new blockchain-based systems and cryptocurrencies [40]. The principles outlined in Nakamoto's whitepaper have influenced the governance and control mechanisms of blockchain technology, shaping its applications in sectors like healthcare, energy, and e-commerce [47]. The whitepaper's innovative concepts have driven the evolution of blockchain technology, enabling enhanced decentralization and security in Web 3.0 applications [48].

The release of the Bitcoin whitepaper in 2008 by Satoshi Nakamoto was a seminal moment that introduced the world to a decentralized digital currency system powered by blockchain technology. This event not only led to the creation of Bitcoin but also catalysed the widespread adoption of blockchain technology across diverse industries, revolutionizing the way transactions are conducted and data is secured. Nakamoto's whitepaper laid the foundation for a new era of decentralized, trustless, and transparent systems that continue to shape the digital landscape today.

The 2010s marked a significant period in the cryptocurrency world with the emergence of alternative cryptocurrencies, commonly known as altcoins, following the success of Bitcoin. These altcoins, such as Litecoin, Ripple, and Ethereum, brought about various innovations aimed at improving upon the limitations of Bitcoin. For instance, Ethereum, introduced in 2015, revolutionized the landscape by introducing smart contracts, which are self-executing contracts with the terms of the agreement directly written into code. This innovation paved the way for decentralized applications (dApps) and the tokenization of assets, expanding the utility of blockchain technology beyond just being a digital currency [49].

Ethereum, in particular, played a pivotal role in advancing the capabilities of blockchain technology by offering a Turing-complete programming language called Solidity for developing smart contracts. This language enabled developers to create complex agreements and applications that could be automatically executed on the blockchain, enhancing the efficiency and security of transactions [49]. The introduction of smart contracts on the Ethereum platform represented a significant leap forward in the evolution of cryptocurrencies, allowing for a wide range of decentralized applications to be built on its network.

Smart contracts, as implemented on platforms like Ethereum, are essentially self-executing contracts with the terms of the agreement directly written into lines of code. These contracts automatically enforce and execute the terms of the agreement when predefined conditions are met, eliminating the need for intermediaries and enhancing the security and transparency of transactions [50]. The decentralized nature of smart contracts ensures that transaction and contract information is open, transparent, and tamper-proof, contributing to a more trustless and efficient system [51].

The rise of Ethereum and its smart contract capabilities led to a surge in research and development focused on analysing and enhancing the security and functionality of these contracts. Various studies have been conducted to evaluate the vulnerabilities and risks associated with smart contracts, aiming to improve their resilience to attacks and exploits [52]. Additionally, tools like SolidityCheck have been developed to quickly detect potential issues in smart contracts through regular expressions, highlighting the importance of ensuring the robustness of these automated agreements [53].

Furthermore, the economic implications of smart contracts, particularly in the context of Ethereum, have been a subject of interest. The execution of smart contracts on the Ethereum blockchain incurs costs in the form of gas, a unit used to measure the computational effort required to process transactions. Understanding the economics behind smart contracts is crucial for optimizing their efficiency and ensuring cost-effective utilization of blockchain resources [54].

In the realm of security, the integrity and protection of smart contracts have been a focal point of research. Tools like ContractGuard have been developed to defend Ethereum smart contracts by embedding intrusion detection mechanisms, safeguarding them against potential threats and vulnerabilities [55]. Ensuring the security of smart contracts is paramount to maintaining the trust and reliability of blockchain-based applications and transactions.

Moreover, the performance and scalability of blockchain platforms supporting smart contracts, such as Ethereum, have been subjects of investigation. Studies have been conducted to analyse the efficiency of blockchain-based smart grids and to compare implementations on platforms like Ethereum and Hyperledger, aiming to enhance the functionality and usability of smart contract applications [56]. Improving the performance of blockchain networks is essential for enabling the widespread adoption of decentralized applications and ensuring seamless user experiences.

The expansion of alternative cryptocurrencies and the introduction of smart contracts in the 2010s have significantly transformed the landscape of blockchain technology. Platforms like Ethereum have spearheaded innovations that go beyond traditional digital currencies, enabling the development of decentralized applications and automated agreements that enhance security, transparency, and efficiency in transactions. The research and development efforts focused on smart contracts underscore the importance of continuously improving their security, performance, and economic viability to unlock the full potential of blockchain technology in the years to come.

The period from 2017 to the present has indeed seen a surge in mainstream attention towards cryptocurrencies, resulting in significant market growth and the introduction of numerous new digital assets through initial coin offerings (ICOs) [57]. This increased interest has not only led to substantial global investments but has also spurred governments and financial regulators worldwide to develop regulatory frameworks to oversee the expanding crypto market [57]. Regulators face the challenge of balancing innovation in the cryptocurrency space with concerns regarding consumer protection, financial stability, and the prevention of illicit activities [57].

Academic research has predominantly concentrated on regulatory aspects and ICOs, while industry articles have placed more emphasis on exchanges and cryptocurrencies themselves [57]. The rise of cryptocurrencies has raised worries about potential illicit activities, particularly money laundering, resulting in varied regulatory responses from outright bans to more inclusive approaches that integrate cryptocurrencies into existing financial regulatory frameworks [58]. The necessity for a comprehensive regulatory framework for cryptocurrencies, including popular options like Bitcoin and Ethereum, has become increasingly evident [59].

Regulatory frameworks play a critical role in shaping the adoption and use of cryptocurrencies by providing clarity on how transactions should adhere to the legal boundaries governing traditional fiat currencies [60]. Inconsistencies in regulations can create uncertainty among users and impede the widespread adoption of cryptocurrencies [14]. Despite the decentralized nature of cryptocurrencies, governments and regulators are actively participating in discussions to establish appropriate frameworks that ensure compliance and mitigate risks associated with digital assets [61].

The regulatory landscape concerning cryptocurrencies varies significantly across different jurisdictions, with some countries advocating for stringent regulations to combat money laundering and terrorist financing, while others are exploring more flexible approaches to accommodate the evolving crypto market [62]. The dynamic nature and high volatility of the cryptocurrency market underscore the importance of regulatory interventions to protect investors and maintain market stability [63]. Additionally, the emergence of new digital assets like Ethereum, Litecoin, and Dogecoin has further emphasized the need for regulatory clarity and oversight [63].

As the cryptocurrency market evolves, there is a growing recognition of the necessity for regulatory frameworks that not only address the unique characteristics of digital assets but also align with existing legal frameworks related to fraud and insider trading [64]. The development of ethical frameworks for responsible AI and machine learning applications in cryptocurrency trading reflects a broader effort to ensure the integrity and transparency of digital asset transactions [64]. By synthesizing existing literature and insights from regulatory experts, policymakers can strive to establish robust regulatory frameworks that promote innovation while safeguarding investors and maintaining market integrity [65].

The increased mainstream attention and regulation of cryptocurrencies from 2017 to the present have marked a significant transformation in the financial landscape, prompting governments, regulators, and researchers to engage in discussions on how to effectively manage the challenges and opportunities presented by digital assets. The establishment of clear and comprehensive regulatory frameworks is crucial to ensure the sustainable growth and integrity of the cryptocurrency market while addressing concerns related to consumer protection, financial stability, and illicit activities.

Central Bank Digital Currencies (CBDCs) have gained significant attention globally, particularly with the rise in popularity of cryptocurrencies. These digital representations of sovereign currencies are being explored by central banks worldwide to leverage blockchain technology for improving payment systems and updating financial infrastructures while ensuring regulatory oversight and stability [66]. While many countries are still in the pilot and research phases of CBDC implementation, some high-income nations have begun cautiously integrating these digital currencies into their economies [67].

Research confirms that CBDCs are essentially digital versions of domestic currencies issued by central banks, with a unit of account equivalent to the respective national currency [68]. The primary objective behind CBDC development is to address potential threats posed by private sector digital currency issuances to monetary policy and financial market stability. Central banks are investigating CBDCs as a means to uphold financial market stability, maintain monetary policy effectiveness, and counter risks [69]. These digital currencies are considered central bank liabilities that can facilitate payments, offering benefits such as reducing financial instability sources, enhancing payment system efficiency and safety, and deterring tax evasion and illicit activities [70].

The exploration of CBDCs is a global trend, with central banks worldwide contemplating the issuance of these digital currencies. The potential advantages of CBDCs include enhancing money demand, optimizing payment systems, expanding the money multiplier effect, and directly influencing monetary policy effectiveness [71]. Additionally, the introduction of CBDCs is viewed as an inevitable progression in the digital finance realm, necessitated by increasing digitalization [72].

A crucial aspect associated with CBDCs is their impact on financial inclusion. Studies suggest that interest-bearing CBDCs could decrease cash demand, promote financial inclusion, and enable holding central bank digital currency without requiring a traditional bank account [73]. Furthermore, CBDCs have the potential to offer improved payment options for financial transactions in the circular economy, fostering greater financial inclusion for unbanked individuals and supporting distressed businesses in the circular economy [74].

While CBDCs offer promise in enhancing financial systems and inclusivity, challenges and considerations exist. Risks associated with CBDC implementation include governance issues, regulatory challenges, interoperability concerns for cross-border payments, and potential impacts on monetary regulation [75]. Central banks are responsible for establishing governance frameworks for CBDCs to ensure effective regulation and mitigate associated risks [76].

The exploration and development of Central Bank Digital Currencies (CBDCs) signify a significant shift in the global financial landscape. These digital representations of sovereign currencies have the potential to transform payment systems, enhance financial inclusion, and modernize monetary policy frameworks. However, the integration of CBDCs into national economies necessitates careful consideration of regulatory, governance, and interoperability aspects to ensure successful implementation and risk mitigation.

Cryptocurrencies are continuously evolving, driven by technological advancements such as decentralized finance (DeFi) applications, stablecoins pegged to traditional currencies, and enhanced scalability solutions [77]. The entry of institutional investors, financial institutions, and technology giants into the crypto space is contributing capital, credibility, and infrastructure that could propel broader adoption and market maturation [77]. Despite these advancements, challenges persist, including regulatory uncertainties, cybersecurity risks, and environmental concerns related to energy-intensive mining practices [77]. However, the promise of digital currencies lies in their potential for financial inclusion, facilitating cross-border payments, and fostering transformative innovations in global finance [77].

The development and adoption of Layer-two solutions are identified as a significant trend aimed at enhancing the scalability and efficiency of blockchain networks [78]. These solutions play a crucial role in addressing the scalability challenges faced by blockchain technologies, making them more viable for widespread use [78]. Additionally, the growing interest in sustainable blockchain solutions and the potential impact of central bank digital currencies are expected to further shape the future of the cryptocurrency ecosystem [77].

Blockchain technology, the foundation of cryptocurrencies like Bitcoin, operates on decentralized principles and cryptographic concepts to provide secure and reliable decentralized solutions [79]. The decentralized nature of blockchain, maintained through proofs-of-work, not only ensures transaction integrity but also serves to generate the monetary supply in cryptocurrencies [79]. Recent advances in blockchain technology have shown significant promise in improving various sectors, including patient care and information management in healthcare [80].

The rise of digital currencies and the underlying blockchain technology has garnered significant attention across various sectors, indicating a growing interest in the potential applications and benefits of these innovations [81]. Blockchain-based decentralized cryptocurrencies have become a focal point of interest and deployment in recent years, reflecting the increasing relevance and adoption of this technology [82]. Decentralized Applications (DApps) built on blockchains provide distributed trusted applications that leverage the security and transparency of blockchain technology [83].

Cryptography forms the fundamental basis of blockchain technology, ensuring the security and integrity of decentralized systems [84]. Innovations such as Zk-SNARKs-based anonymous payment channels aim to enhance transaction speeds in cryptocurrencies, enabling high-frequency transactions on a global scale [85] The integration of cryptography in blockchain systems is essential for ensuring the privacy and security of transactions, especially in scenarios like secure e-voting systems [86].

Efforts to address scalability issues in blockchain systems have led to the exploration of solutions like sharding, cooperative mining systems, and demand-aware payment channel networks [87-89]. These approaches aim to improve the scalability and efficiency of blockchain networks, making them more capable of handling increased transaction volumes and diverse application domains [87-89]. Additionally, research on blockchain storage, scalability, and availability underscores the importance of these aspects in ensuring the robustness and sustainability of blockchain systems [90].

As the adoption of cryptocurrencies continues to grow, the scalability of blockchain technologies has become increasingly crucial for their widespread acceptance and utility [91]. The scalability challenges faced by blockchain systems are being addressed through various mechanisms, including off-chain transactions, payment channel networks, and sharding techniques [91-93]. These solutions aim to enhance the performance and scalability of blockchain networks, making them more efficient and adaptable to evolving demands [91-93].

The potential applications of blockchain technology extend beyond cryptocurrencies to areas like supply chain management, genomics, and Internet of Things (IoT) integration [94-96]. Blockchain's role in enhancing traceability, security, and transparency in supply chains has positioned it as a transformative technology for modern supply chain operations [94]. Moreover, the integration of blockchain in genomics and IoT systems highlights its versatility and potential to revolutionize diverse industries [95, 96].

The current trends in cryptocurrencies and blockchain technology reflect a dynamic landscape characterized by ongoing innovations, increased institutional involvement, and a focus on scalability and efficiency improvements. While challenges such as regulatory uncertainties and cybersecurity risks persist, the transformative potential of digital currencies in fostering financial inclusion and driving global financial innovations remains promising. The future outlook for cryptocurrencies and blockchain technology hinges on continued advancements in scalability solutions, sustainable blockchain practices, and the exploration of new applications across various sectors.

Decentralization, Blockchain, and Cryptography

Decentralization

Decentralization in the context of cryptocurrency refers to the fundamental principle that underpins many cryptocurrencies, including Bitcoin and Ethereum. It encompasses several key aspects that differentiate these digital currencies from traditional centralized financial systems:

Key Aspects of Decentralization in Cryptocurrency:

Decentralized Ledger (Blockchain): Cryptocurrencies operate on decentralized ledgers, typically known as blockchains. A blockchain is a distributed database maintained by a network of computers (nodes) spread across the globe. Each node stores a copy of the entire blockchain, and all nodes work together to validate and record transactions in blocks.

Peer-to-Peer Transactions: Cryptocurrencies enable direct peer-to-peer transactions without intermediaries like banks. Users can transfer funds directly to each other across the network without relying on a central authority to facilitate or verify transactions. This decentralization reduces transaction costs and eliminates the need for traditional financial institutions.

Consensus Mechanisms: Decentralized consensus mechanisms ensure agreement among network participants regarding the validity of transactions and the state of the ledger. Bitcoin, for example, uses Proof of Work (PoW), where miners compete to solve complex mathematical puzzles to add new blocks to the blockchain. Ethereum is transitioning to Proof of Stake (PoS), where validators are chosen to create new blocks based on the number of coins they hold.

Immutable and Transparent Transactions: Transactions recorded on a blockchain are immutable, meaning they cannot be altered or deleted once confirmed. This transparency ensures that all transaction history is publicly verifiable, enhancing trust among participants and reducing the risk of fraud or manipulation.

Censorship Resistance: Decentralized cryptocurrencies are resistant to censorship and control by any single entity or government. This feature is particularly valuable in regions with unstable financial systems or limited access to traditional banking services, where cryptocurrencies can provide financial freedom and inclusion.

Decentralization in cryptocurrency signifies a significant departure from traditional financial systems by distributing control and authority across a network of participants rather than consolidating power in a central entity. This transformative concept is exemplified by cryptocurrencies like Bitcoin and Ethereum, which operate on decentralized ledgers known as blockchains. These blockchains are distributed databases maintained globally by nodes, with each node storing a complete copy of the ledger, ensuring transparency and resilience [97]. Transactions within these cryptocurrencies are grouped into blocks, validated through consensus mechanisms, and added to the chain chronologically, eliminating the need for a central authority to manage transaction records and ensuring data integrity and security through cryptographic techniques [97].

A pivotal aspect of decentralization in cryptocurrency is the facilitation of peer-to-peer transactions, enabling users to engage in direct transactions without intermediaries such as banks. This direct interaction through cryptographic keys allows for seamless and efficient fund transfers globally, bypassing the traditional banking infrastructure and reducing transaction costs associated with intermediaries [97]. Furthermore, decentralized cryptocurrencies rely on consensus mechanisms to validate transactions and uphold the integrity of the blockchain. For instance, Bitcoin utilizes Proof of Work (PoW), where miners compete to solve complex mathematical puzzles to validate transactions and create new blocks, while Ethereum is transitioning to Proof of Stake (PoS), where validators are chosen based on the amount of cryptocurrency they hold, enhancing security and efficiency while reducing energy consumption compared to PoW [97].

Moreover, the immutability and transparency of transactions recorded on a blockchain are critical aspects of decentralization in cryptocurrency. Once transactions are confirmed and recorded on the blockchain, they become immutable, meaning they cannot be altered or deleted. This transparency enhances trust among participants as transaction history is publicly verifiable, reducing the risk of fraud or manipulation [97]. Additionally, decentralized cryptocurrencies exhibit resistance to censorship and control by any single entity or government, providing individuals in regions with unstable financial systems or limited access to traditional banking services with financial freedom and inclusion [97].

Decentralization in cryptocurrency not only revolutionizes financial systems but also offers various advantages such as broadening financial inclusion, encouraging permission-less innovation, eliminating the need for intermediaries, ensuring transaction immutability, and enabling censorship resistance. These benefits are highlighted in the literature, emphasizing the positive impact of decentralized finance on the global financial landscape [98]. Furthermore, the decentralized nature of cryptocurrencies like Bitcoin has been associated with facilitating the transition to renewable energy, demonstrating the broader implications and applications of decentralized systems beyond financial transactions [99].

In the realm of blockchain technology, which underpins decentralized cryptocurrencies, various studies have explored the attack surface of blockchain, underscoring the importance of effective defence measures to mitigate vulnerabilities and attacks [97]. Additionally, research has delved into the security analysis of cryptocurrencies based on blockchain technology, emphasizing the critical role of blockchain in maintaining the security and integrity of cryptocurrencies [100]. The utilization of blockchain technology has extended beyond cryptocurrencies to advance smart cities, enabling reliable and transparent data exchange without the need for centralized administrators [101].

Furthermore, the development of decentralized applications (dApps) has expanded the capabilities of decentralized systems, facilitating activities such as voting systems and treasury management within decentralized autonomous organizations (DAOs) [102]. The governance structures of decentralized financial market infrastructures, such as Bitcoin, have been scrutinized, shedding light on the decentralized nature of these systems and their significance in the financial realm [103]. Additionally, the potential for utilizing public blockchains for censorship-circumvention and IoT communication has been explored, showcasing the versatility and adaptability of blockchain technology in various domains [104].

Advantages of Decentralization in Cryptocurrency:

Security: Decentralization reduces the risk of single points of failure and enhances the security of transactions and user funds. Attackers would need to compromise a significant portion of the network to manipulate transactions, making such attacks economically impractical.

Trustlessness: Participants can interact and transact without needing to trust each other or third-party intermediaries. Cryptographic protocols and consensus mechanisms ensure that transactions are valid and secure without requiring trust in a central authority.

Global Accessibility: Anyone with internet access can participate in the cryptocurrency network, send and receive funds, and engage in financial activities without geographic restrictions or the need for traditional banking infrastructure.

Decentralization in cryptocurrency offers several key advantages that contribute to the security, trustlessness, and global accessibility of these digital assets. One significant benefit of decentralization is the enhanced security it provides by mitigating the risk of single points of failure within the network [105]. This decentralized structure makes it economically impractical and highly secure for attackers to compromise a significant portion of the network to manipulate transactions, thereby safeguarding user funds and transaction integrity [105]. Furthermore, decentralization fosters trustlessness by enabling participants to transact without the need to trust each other or rely on third-party intermediaries [106]. Cryptographic protocols and consensus mechanisms ensure the validity and security of transactions, eliminating the necessity for trust in a central authority and promoting a trustless ecosystem [106].

Moreover, decentralization in cryptocurrency networks facilitates global accessibility, allowing anyone with internet connectivity to participate in financial activities without geographical restrictions or dependence on traditional banking infrastructure [14]. This inclusivity promotes financial empowerment and economic participation on a global scale, democratizing access to financial services and opportunities [14]. The decentralized nature of cryptocurrencies, such as Bitcoin, introduced by Satoshi Nakamoto in 2008, has revolutionized the financial landscape by offering a secure and decentralized alternative to traditional centralized systems [107]. The decentralized feature of cryptocurrencies like Bitcoin ensures that no central authority can impose taxes, providing users with a level of financial autonomy and privacy [108].